China has enacted its recently revised individual income tax law, a big overhaul of the law over more than 30 years from its inception.

Some of the changes will be set to have an impact on you, either foreigners or oversea Chinese.

1. New Definition of Tax Residents

In the prior version of the IIT law, a tax resident is one who has domicile within China or otherwise lives within China up to one year, and a person who does not have domicile and doesn't live within China, or who, without domicile, lives within China not up to one full year, is not a China resident for purpose of IIT.

Now in the new IIT law, the one year stay requirement is shortened to 183 days within a tax year. With the new change, more foreigners or oversea Chinese working within China will be caught by this law.

|

Definition |

Requirement of Stay |

Tax Scope |

| Resident | China-domiciled individuals;or

Non-China-domiciled individuals who stay in China for 183 days or more in a calendar year

|

Worldwide income |

| Non-Resident | Non-China-domiciled individuals who stay in China for less than 183 days in a calendar year

|

Only China-sourced income |

It remains to see whether the previous five-year rule will continue to apply to foreigner employees, namely, if a foreigner without domicile in China has been working in China for more than five consecutive full years, then he is subject to IIT for his worldwide income.

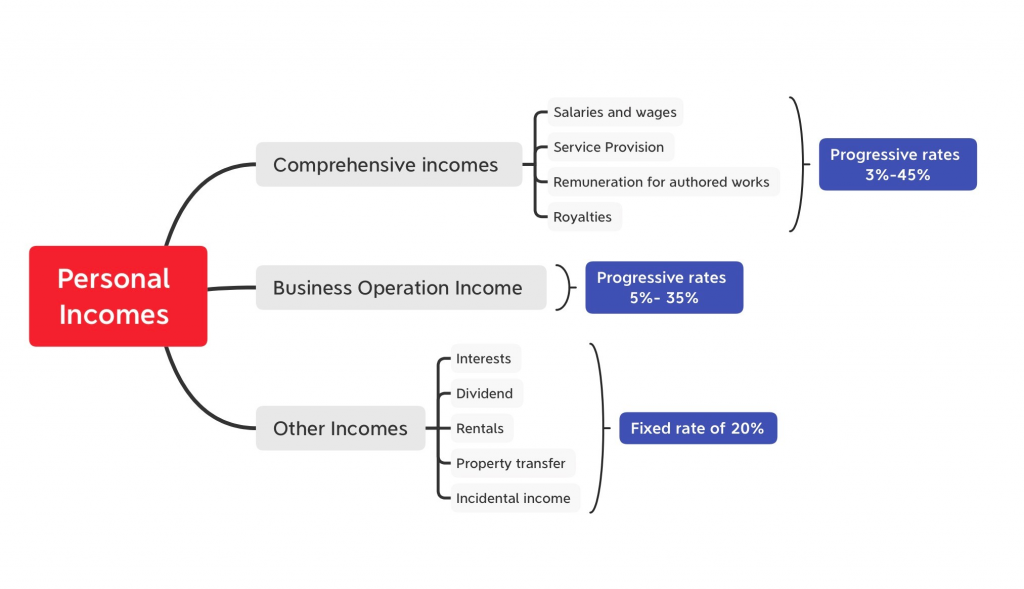

2. Introduction of Comprehensive Income and Specific Additional Deducible Concepts

The old law applied the progressive rates of 3%-45% only to salaries and remunerations paid for employment but now these rates are applies to four types of income consolidated together as "comprehensive income", expanding beyond original salaries and remunerations to include incomes derived from service provision, writing (meaning people earning income by writing articles, books or essays etc.), and royalties.

To make taxation more equal and fair, in addition to the general standard deductibles such as monthly RMB 5000 and social security contributions, the Law now allows specific additional deductibles such as children education, continuous education, medication of serious illness, interest on mortgage loans (or rental paid for residence) as well as cost for supporting elderly family members. As for how exactly these deductibles will be implemented, detailed rules will be released for sure.

3. Anti-Avoidance Rules

It has been an open secret that many Chinese rich people have learned to hide their income and avoid taxes imposed under IIT law. The new law is revised to tackle this tax avoidance.

Article 8 provides that in the following circumstances tax authority shall have the power to adjust the taxation:

(1) When transactions between an individual and his/her affiliated or related parties do not comply with the arm’s length principle and the noncompliance cannot be justified;

(2) When a resident individual controls (or jointly controls with other resident enterprises) an enterprise established in a jurisdiction where the effective tax rate is significantly low and the enterprise does not distribute profits or distributes less profits than it should without a reasonable business justification; and

(3) When an individual obtains improper tax benefits through an arrangement that lacks a reasonable business purpose.

Upon adjusting the taxation, penalty interests will be imposed as well.

4. Implications on Foreigners Working in China

(1) With the new IIT law, more foreigners working in China will be subject to China individual income tax law, and given the relatively high tax rate of 45%, the new law has a chilling effect on multi-national corporations that want to send expats to work in China.

(2) Before this new law, an individual without domicile in China enjoys a special favorable treatment of additional standard deduction of RMB 1300 every month from his or her salaries and wages. However, the new law has repealed the additional standard deduction of RMB 1,300 per month that currently applies to salaries and wages earned by foreign individuals working in China and China-domiciled individuals working overseas.

In Article 6 of the new IIT Law, it says "the balance of monthly salaries and wages minus RMB 5000 shall be the taxable income for non-resident taxpayer. Actual income earned in each transaction from services provision, writing and royalties shall be the taxable income under IIT law.

While it seems more equal and fair to bring foreigners under the same rules, it could actually be biased and unfair to foreign employees who work in China and fall within the tax residents definitions, as it will be much more difficult for them to present those newly introduced specific additional deductions that may be incurred outside of China.

(3) It remains unclear at this stage whether China will further take away those benefits that have been offered to foreign employees in China, such as housing and food subsidy, language training fee, approved children education fee and dividend emanating from investment in foreign-invested enterprises.

5. Tax Clearance upon Emigration (Oversea Chinese)

For the first time, China in its IIT law requires tax clearance by Chinese citizens that emigrates abroad and deregister his or her Hukou (household registration in China).

In reality, many Chinese emigrating abroad (even after being naturalized) but still keep their China Hukou that signifies his or her status as a Chinese citizen.

Now with the new rule, if a Chinese citizen wishes to deregister their Hukou, she or he shall settle and liquidate her or his tax liabilities within China.

This will mostly impact those oversea Chinese who acquire permanent residence abroad and want to take money out of China. Under the current China rules concerning transfer of assets out of China, the Chinese person shall present evidence of revocation of their Hukou with local police office. Now with this new requirement on tax clearance, it remains to be seen what this really means in practice.

We have advised clients (oversea Chinese) in moving their property sale proceeds out of China. As part of the documentation for application for approval from local foreign exchange authority, we need to submit the tax invoices (fapiao) to prove that relevant taxes in regard of the sale proceeds have been duly paid. But this is just tax clearance in respect of certain piece of assets, and the new rule may be constructed as to mean overall tax clearance by that person of all dealings made by him or her before the emigration.

Comments